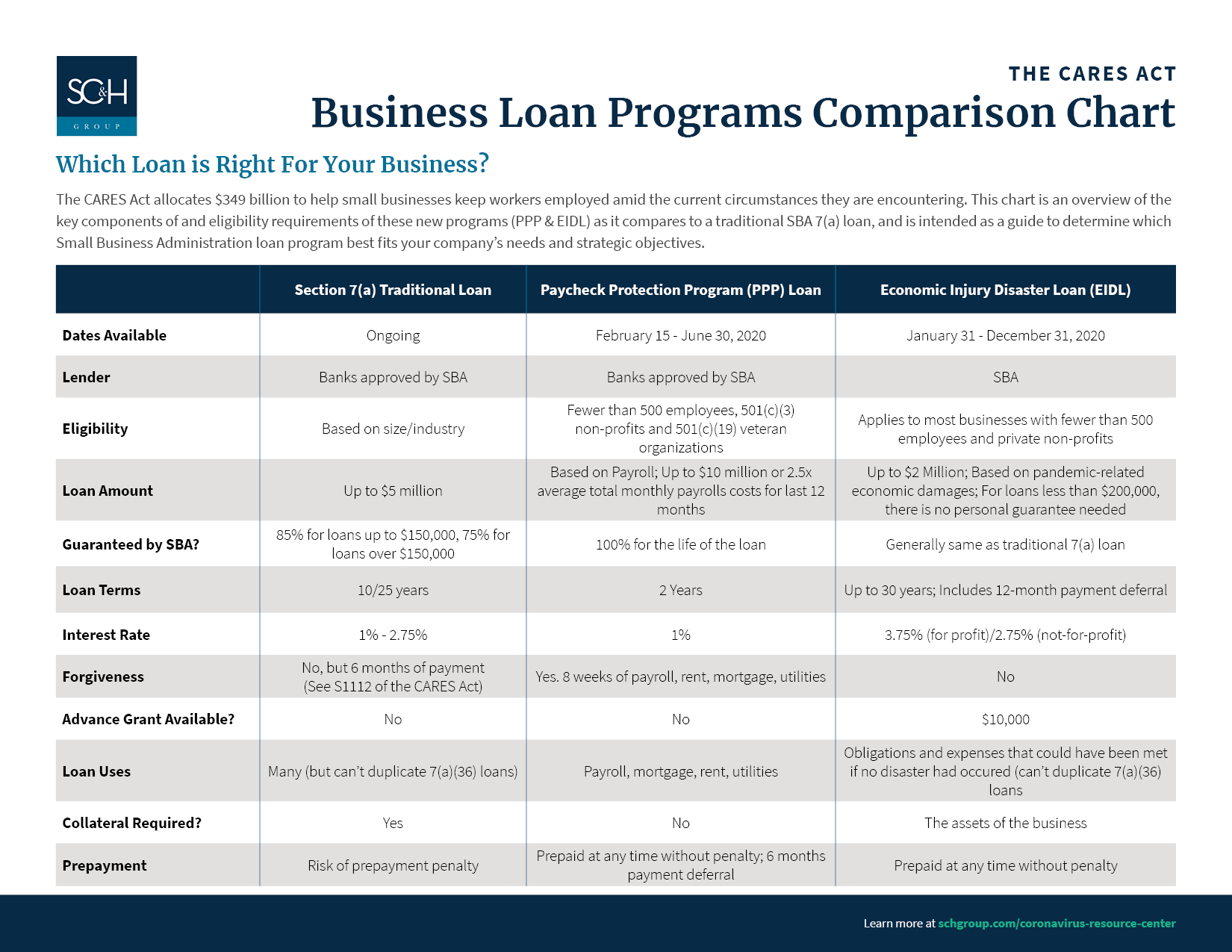

Advice for first-time loan applicants in 2025. As you embark on the journey of securing your first loan, it’s essential to navigate this process with clarity and confidence. The world of loans can be overwhelming, especially for newcomers, but understanding the landscape and preparing adequately can make all the difference. Whether you’re eyeing a personal loan, mortgage, or student loan, this guide will provide you with the insights needed to approach loan applications successfully.

First-time applicants will learn about different loan types, the importance of financial documentation, and how to effectively research lenders. We’ll also cover managing expectations throughout the application process and what to focus on after approval. Let’s dive into these essential tips and set you up for success.

Understanding Loan Types

When considering a loan for the first time, it’s essential to grasp the various loan types available. Each type of loan comes with its characteristics, terms, and purposes, which can significantly impact your borrowing experience. Understanding these differences will help you make informed decisions tailored to your financial needs.There are primarily two categories of loans: secured and unsecured loans. Secured loans require collateral, such as a home or a car, which reduces the lender’s risk.

On the other hand, unsecured loans do not require collateral and are based on the borrower’s creditworthiness. Each type has its advantages and disadvantages that are critical to understand before submitting an application.

Types of Loans

The following are common types of loans that first-time applicants might encounter, along with their specific traits:

- Personal Loans: These are unsecured loans used for various purposes, like debt consolidation or unexpected expenses. They typically have fixed interest rates and repayment terms. However, interest rates can be higher compared to secured loans.

- Mortgages: These are secured loans specifically for purchasing real estate. The property itself serves as collateral. Mortgages often offer lower interest rates due to the security provided by the asset, but they involve long-term commitments and extensive paperwork.

- Student Loans: Designed to cover education costs, these loans can be federal or private. Federal student loans often have lower interest rates and more flexible repayment options, while private loans might require credit checks and can have variable rates.

Understanding the pros and cons of secured versus unsecured loans can help you determine which option is preferable based on your financial situation. Secured loans may offer lower interest rates and larger borrowing amounts, but the risk is that you could lose your collateral if you default. Unsecured loans typically carry higher interest rates, but they do not risk your assets in the same way.

“Choosing the right loan type is crucial for your financial health and future stability.”

Being aware of these aspects will equip first-time loan applicants with the knowledge necessary to navigate the lending landscape effectively. Each loan type has its unique features, and knowing them can lead to better financial decisions that align with personal goals and capabilities.

Preparing Financial Documents

When applying for a loan, having the right financial documents is crucial for a smooth application process. It not only streamlines your interaction with lenders but also plays a significant role in determining your loan eligibility and terms. This section will cover the essential documents you’ll need, the importance of your credit score, and how you can better organize your application materials.

Key Financial Documents Required

Gathering the necessary financial documents can seem overwhelming, but it’s essential to present a complete picture of your financial health to lenders. The following documents are typically required when applying for a loan:

- Proof of Income: Recent pay stubs or tax returns to verify your income. This shows lenders your earning capacity.

- Bank Statements: Usually, the last three to six months of bank statements are needed to show your savings and spending habits.

- Credit Report: A comprehensive report detailing your credit history, outstanding debts, and payment history. This is crucial for assessing your creditworthiness.

- Employment Verification: A letter from your employer confirming your position and salary, which helps to ensure job stability.

- Debt Statements: Documentation of any existing loans or credit card debt to give a full picture of your financial obligations.

- Identification: A government-issued ID or passport is usually required to verify your identity.

Importance of Credit Scores

Understanding your credit score is critical in the loan application process. Your credit score reflects your creditworthiness and influences the interest rates and terms lenders may offer you. Higher credit scores generally lead to better loan conditions, so knowing how to improve your score can be beneficial.

“Lenders often use credit scores to gauge the risk of lending to you; a higher score can mean lower interest rates.”

Common strategies to improve your credit score include:

- Paying bills on time to maintain a positive payment history.

- Keeping credit utilization below 30% of your total available credit.

- Avoiding opening multiple new credit accounts in a short period, which can raise red flags for lenders.

- Regularly checking your credit report for errors and disputing any inaccuracies found.

Document Organization Checklist

Having an organized checklist can simplify your loan application process significantly. Below is a checklist to help you gather and organize your financial documents effectively.

- Proof of Income (pay stubs, tax returns)

- Recent bank statements

- Credit report

- Employment verification letter

- Debt statements

- Government-issued ID

By ensuring you have these documents ready and organized, you can approach the loan application process with confidence, increasing your chances of approval.

Researching Lenders

When applying for a loan, selecting the right lender is critical for securing the best terms and ensuring a smooth borrowing experience. With various lending options available, it’s essential to perform thorough research to find a lender that fits your needs and financial situation. This step not only enhances your likelihood of approval but also empowers you to make informed decisions regarding interest rates, repayment terms, and overall loan conditions.Comparing lenders effectively requires a strategic approach that incorporates several methods.

Begin by identifying multiple lenders that offer the type of loan you’re seeking, whether it’s a personal loan, mortgage, or student loan. Utilize comparison websites that aggregate information from various lenders, allowing you to see the differences in interest rates, fees, and terms side by side. Moreover, reaching out to local credit unions and banks can provide insight into personalized loan options that may not be reflected on broader comparison sites.

Significance of Online Reviews and Ratings

Online reviews and ratings can play a pivotal role in the decision-making process when selecting a lender. These reviews provide firsthand accounts from previous borrowers, offering insights into the lender’s customer service, responsiveness, and overall reliability. High ratings generally indicate a satisfactory experience, while consistent negative feedback may signal potential red flags. Consider the following factors when evaluating online reviews:

- Volume of Reviews: A higher number of reviews can provide a more balanced perspective on the lender’s reputation.

- Recency of Reviews: Recent reviews reflect the current service standards and operational practices of the lender.

- Detailed Feedback: Look for specific comments about the loan application process, transparency of fees, and customer support experiences.

Questions to Ask Potential Lenders, Advice for first-time loan applicants in 2025.

During consultations with potential lenders, asking the right questions is essential to gain a clear understanding of their offerings. Here are key inquiries to consider that will help you assess each lender’s suitability for your needs:Begin your list with inquiries that delve into the lender’s processes and product specifics:

- What types of loans do you offer, and which would best suit my situation?

- What are your current interest rates, and how are they determined?

- Can you explain your fee structure in detail?

Additionally, address their customer service and support capabilities:

- What resources do you provide to help me understand the loan process?

- How accessible is your customer support for questions during the loan term?

- What happens if I miss a payment?

Finally, inquire about the logistics of the loan itself to better prepare for the commitment:

- What is the expected timeline for loan approval and funding?

- Are there any prepayment penalties associated with this loan?

- Can I make additional payments without penalty?

Managing Expectations

Navigating the world of loans can be overwhelming, especially for first-time applicants. One of the key aspects to focus on is managing your expectations throughout the application process. Understanding what to anticipate can help you prepare more effectively and reduce anxiety as you move forward in securing your loan.

When applying for a loan, it’s essential to have realistic timelines in mind regarding approval and disbursement. The approval process can take anywhere from a few days to several weeks, depending on various factors such as the lender’s requirements and the complexity of your financial situation. After approval, disbursement can occur as quickly as one business day or take longer based on the lender’s policies.

It’s wise to plan for potential delays, as factors like incomplete documentation or verification issues can lead to longer processing times.

Common Reasons for Loan Application Rejections

Several factors can lead to a loan application being rejected, and recognizing these can help you prepare better. Here are some prevalent reasons applicants face denials:

- Low Credit Score: Many lenders require a minimum credit score. A low score may indicate risk, leading to rejection.

- Insufficient Income: Lenders need to see that you can repay the loan. If your income is too low compared to your expenses, this can be a red flag.

- High Debt-to-Income Ratio: A high ratio suggests that you may already be over-leveraged, making lenders wary.

- Incomplete Documentation: Missing paperwork can stall or doom an application, as lenders require thorough verification.

- Employment History: A lack of stable employment or frequent job changes can make lenders hesitant.

Preparing for potential challenges during the application process is essential for a smoother experience. Here are strategies to consider:

Strategies to Prepare for Application Challenges

Understanding common challenges helps you create a proactive approach. Here are some strategies to mitigate issues:

- Improve Your Credit Score: Check your credit report well in advance and address discrepancies. Aim to improve your score by paying down debts.

- Gather Complete Documentation: Prepare and organize essential financial documents, including pay stubs, tax returns, and bank statements, before applying.

- Calculate Your Debt-to-Income Ratio: Assess your finances to understand your current ratio and take steps to lower it if necessary.

- Maintain Stable Employment: If possible, try to stay in the same job for at least six months before applying to show stability.

- Communicate with Lenders: Be upfront with lenders about your financial situation; this transparency can help them guide you through the process.

Remember, a solid understanding of these expectations and challenges is critical to navigating your first loan application successfully.

Understanding Loan Terms and Conditions

When applying for a loan, it’s crucial to grasp the terms and conditions that come with it. Understanding these elements not only helps you make informed decisions but also prepares you for the financial commitments ahead. This section will shed light on essential loan vocabulary and how to interpret loan agreements, ensuring you know exactly what you’re signing up for.

Essential Loan Terms

Familiarizing yourself with key loan terminology is vital for comprehending your financial obligations. Here are some essential terms you should know:

- APR (Annual Percentage Rate): This represents the yearly cost of borrowing, including interest and any additional fees. Understanding the APR helps you compare loans effectively, as it reflects the total cost of the loan.

- Amortization: This refers to the process of paying off a loan over time through regular payments. An amortization schedule Artikels how much of each payment goes toward interest and principal. Knowing your amortization timeline helps you plan your financial future.

- Collateral: This is an asset pledged by the borrower to secure a loan. If the borrower defaults, the lender can claim the collateral. Common forms of collateral include real estate or vehicles, and understanding its role can influence your loan choices.

Fixed-rate vs Variable-rate Loans

Understanding the differences between fixed-rate and variable-rate loans is crucial as it can significantly impact your financial strategy.

- Fixed-rate loans

- Variable-rate loans, on the other hand, have interest rates that can fluctuate based on market conditions. This means your payments could increase or decrease over time. For instance, a variable-rate loan might start at 3% but could rise to 5% if market rates increase, potentially leading to higher monthly payments.

Interpreting Loan Agreements

Reading and understanding loan agreements is a critical step in the loan application process. These documents can be complex, but breaking them down into manageable parts can improve comprehension.Begin by looking for the following sections:

- Loan Amount: This specifies how much money you are borrowing. Ensure this aligns with your needs and financial plan.

- Repayment Terms: This Artikels the duration of the loan and the payment schedule. Knowing the term length helps you understand how long you’ll be making payments.

- Fees and Penalties: Look for any mention of origination fees, late payment penalties, or prepayment penalties. Being aware of these can prevent unexpected costs.

- Conditions for Default: This section details what constitutes default and the consequences. Understanding this can help you stay vigilant in your repayment efforts.

“Thoroughly reviewing loan agreements ensures you are not only aware of your obligations but also protects you from potential pitfalls.”

Building a Strong Application

Crafting a strong loan application is crucial for first-time applicants looking to secure funding. A robust application can significantly increase your chances of approval and help you obtain favorable terms. This section covers essential strategies to enhance your application, tips for writing a compelling personal statement, and how to leverage local community resources effectively.

Strategies to Enhance the Strength of a Loan Application

A strong loan application requires careful preparation and attention to detail. Here are key strategies to enhance your application:

1. Check Your Credit Score

Understanding your credit score is vital, as it directly impacts lender decisions. A score above 700 is generally considered favorable.

2. Reduce Debt-to-Income Ratio

Aim for a debt-to-income ratio below 36%, as this suggests you can manage additional debt comfortably.

3. Provide Accurate Information

Ensure all information is complete and accurate. Any discrepancies can lead to delays or denials.

4. Highlight Stable Income

Document consistent income sources, such as employment or business revenue, to demonstrate repayment capability.

5. Include Collateral

If applicable, offering collateral can strengthen your application by reducing lender risk.

6. Seek Co-signers

A co-signer with strong credit can enhance your application’s attractiveness, especially if your credit history is limited.

Tips for Writing a Personal Statement

A well-crafted personal statement can set your application apart from others. Here are some tips to consider when writing yours:

Be Authentic

Share your genuine story. Explain why you need the loan and how it will positively impact your life.

Stay Concise

Keep your statement focused, ideally within 500 words. Clear and concise writing is more effective than lengthy explanations.

Highlight Financial Responsibility

Discuss past experiences that demonstrate your ability to manage finances, such as budgeting or saving for a specific goal.

Express Future Goals

Articulate your short-term and long-term financial goals, showing lenders that you have a vision for your financial future.

Proofread

Review your statement for grammar and spelling errors. A polished statement reflects attention to detail and professionalism.

Leveraging Local Community Resources

Local community resources can provide valuable assistance when applying for a loan. Here’s how to leverage them effectively:

Financial Literacy Programs

Many communities offer workshops on budgeting, credit management, and loan applications. Participating in these can enhance your knowledge and confidence.

Non-profit Credit Counseling

Seek guidance from non-profit organizations that offer free credit counseling services. They can help you understand your credit report and develop a plan to improve your score.

Local Banks and Credit Unions

These institutions may have specific programs for first-time borrowers. They often provide personalized service and may be more flexible than larger banks.

Community Development Financial Institutions (CDFIs)

CDFIs focus on providing loans to underserved communities. They may offer favorable terms and support for individuals with less-than-perfect credit.

Workforce Development Agencies

If you’re seeking employment or career advancement, these agencies can provide resources to help you increase your income, thereby strengthening your loan application.By focusing on these strategies, personalizing your statement, and utilizing community resources, you can build a strong loan application that stands out to lenders.

Post-Approval Responsibilities

Once your loan has been approved, the journey doesn’t end there. It’s essential for borrowers to understand their responsibilities following loan approval to maintain financial health and good credit standing. This stage involves diligent planning and consistent management of repayments, which is critical for long-term financial success. Timely repayment of your loan is not just a matter of meeting obligations; it directly influences your credit score and overall financial reputation.

A good credit score can lead to better interest rates on future loans, while missed or late payments can severely impact your financial standing. It’s crucial to establish a structured plan for managing your monthly repayments effectively.

Impact of Timely Repayments

Timely repayments serve as a cornerstone for maintaining a healthy credit score. The following points highlight the importance of adhering to your repayment schedule:

- Positive Credit Reporting: Regular, on-time payments are reported to credit bureaus, improving your credit history.

- Lower Interest Rates: A strong credit score can qualify you for lower rates on future loans, saving you money.

- Loan Approval Ease: Good repayment habits make you a more attractive borrower, simplifying future loan applications.

To effectively plan your monthly repayments, it’s advisable to create a budget that accommodates these obligations without stretching your financial limits. Here are some strategies for successful budgeting:

Budgeting for Monthly Repayments

Budgeting is essential for ensuring that you can meet your loan repayments without strain. Implementing a solid budgeting strategy can simplify this process.

- Track Your Income: List all sources of income to understand your total earnings each month.

- Identify Fixed Expenses: Catalog all fixed expenses, including rent, utilities, and existing debt payments, to gauge available funds.

- Allocate for Loan Repayment: Designate a specific portion of your income for loan repayment each month, prioritizing it within your budget.

- Monitor Spending: Keep track of discretionary spending and adjust as necessary to ensure loan payments remain manageable.

“Creating a budget is not about restricting yourself; it’s about making your money work for you.”

By staying proactive and organized, you can maintain your loan obligations without compromising other financial goals. This diligence not only supports your current financial situation but also lays a solid foundation for future borrowing opportunities.

Top FAQs: Advice For First-time Loan Applicants In 2025.

What types of loans are available for first-time applicants?

First-time applicants can consider personal loans, mortgages, and student loans, each with distinct features and requirements.

How can I improve my credit score before applying?

Improving your credit score can be achieved by paying off debts, making timely payments, and checking your credit report for errors.

What should I look for when comparing lenders?

Look for competitive interest rates, favorable terms, customer service reputation, and online reviews when comparing lenders.

How long does it typically take to get loan approval?

The timeline for loan approval can vary but generally takes anywhere from a few days to several weeks depending on the lender and loan type.

What are my responsibilities after loan approval?

Post-approval, it’s crucial to understand your repayment schedule, manage your budget effectively, and ensure timely repayments to maintain a good credit record.